Britain, partly on account of its preeminent financial center in the City, may be the only advanced country positioned to move to a new socio-economic model.

Any country proposing to make an even moderately radical break from the status quo will face deep scepticism from the establishment, and the establishment today is embodied in the international financier and the global corporation, on whom the peace of our societies and the satisfactions of the great majority are now dependent.

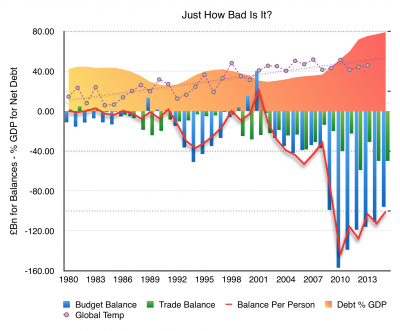

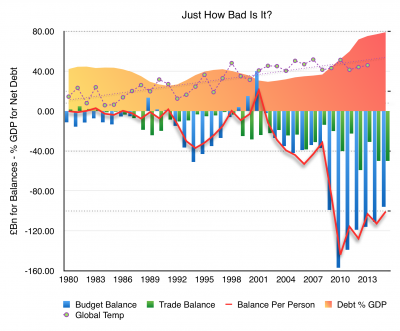

Our current system already rides a razor-thin line between plausibility and fantasy with never-seen-before levels of debt and monetary adventurism, the credibility of which are predicated on long term projections of growth and stability that beggar the imagination.

Any new ideas for how to structure our political economy must either promise to conform to the tightrope we are on, or provide a credible alternative. Any plan that increases spending or investment but does not raise new revenues must necessarily be dependent on some combination of growth, debt, or monetary expansion. Given the already stretched boundaries of the current construct, notions of higher levels of growth, debt, or monetary expansion can only be dependent on justifications that amount to postulation. What seems certain, and to which Greek politicians can attest, is that no country without control of its own currency and direct access to an international financial centre would be able to entertain deviating from the path of the status quo.

It is the very precariousness of the status quo that lends weight to the admonitions of the establishment, embodied in the advice doled out by Germany (through the Eurogroup) and the world’s financial überinstitutions. They are, rightly, deeply sceptical of novel approaches that refuse to adhere to the established limits of fiscal and economic boundaries, because the precious commodity of confidence that underpins the entire system is not within their direct control and rests on a generalised acceptance of models that use historical basis as their justification.

Thrust thus into the seemingly concrete confines of fiscal and economic rules that prescribe that “there is no alternative” (TNA), there are some that divine an escape route through the use of the very tools that support the status quo, and favourite amongst those is monetary adventurism, mostly in some form of “quantitive easing”. Primarily a despondent and confused left, but also an angry and careless right, are gravitating to justifications for their expansionist promises that rely on the use of the same growth, debt, and monetary adventurism that their nemeses already deploy. Irrespective of the quality of their arguments, what is evident is that their ideas are dependent for practical application on the existing financialisation of the economy. This new gloss on old ideas betrays their plans as contradictory to the analysis that they use to substantiate their intentions. If the current malaise is substantially explained by the financialisation of the political economy over the last 30 years, how can the remedy be to lean further on that same system to justify investment? If we are destroying the planet with our growth based models for advancement, how can it be a solution to devise new systems that are ever more dependent on further growth? If expanded debt has substituted for fiscal rectitude, how can more debt, justified by more growth, help to retrieve balance in our affairs?

This then is the root corruption at the base of the supposedly new models we are offered today: that they are at once a critique of the status quo, and they then lean on the established structures to enable their proposed remedies. They cannot stand, and they will face the same fate as Greece: to be subjugated to the established structures, or face penury and exclusion, lest they unbalance the precarious justifications used in the rest of the system by the rest of the world. This is not cruel punishment, this is simply self preservation by the majority.

No model that will not simultaneously increase public revenues and balance that burden with an increase in the quality of life of the great majority can walk away from the established constructs. If the model depends on the existing structures but refuses to accept the strictures of that regime it will be, and must be, frozen out when it comes to implementation.

Moving on from the vanities of the shallow philosophies of the new left and the new right, what of the possibilities for proper change? What of the fate of a properly constructed new political economy, wherein the fiscal logic is not dependent on infinite growth, debt, or monetary adventurism? Such a concept would also have to face the realities of the status quo, and navigate a future in which the rest of the world remained to be convinced of such a path. This could only be achieved in a society which had control of its own currency and direct access to a domestic financial market with sufficient depth and strength to weather the early phase of establishment. Otherwise the maintenance of the inherited debt would quickly overwhelm the nascent reconstruction. This substantial hurdle would be insurmountable in all except a very few countries, and amongst those possibly only the UK has the demos and the institutional fabric strong enough to make it happen.

Britain could lead the way and do what others want to do, but cannot do, because we host the institutional fabric necessary to enable change independently. There is a world of difference between proposing a fiscally balanced future that only needs to maintain the existing debt load, and a proposal to exacerbate the existing paradigm as a means of reaching a promised future. The sanctity of government bonds rests in the ultimate power of a state to raise taxes, which is the resorting guarantee behind the economic projections of any particular administration. If the financial markets have convinced themselves that the current debts are sustainable on the current projections then any new plan that incorporates raising the revenues to pay for its proposals leaves the current status unruffled. There would remain any number of underlying assumptions that a new plan would have to leave undisturbed, and that is where a strong domestic financial market becomes important. The critical impact of a judgement to sustain continued credibility, versus the costs of concluding otherwise, is only likely in a country that has monetary independence and a deeply integrated financial system. For those reasons Britain is uniquely placed to make the move to a more sustainable and joyful political economy, and to benefit from the first mover advantages.

Completing the next phase of the post 1945 settlement by extending the same principles embodied in the NHS to a complete range of basic life supporting services is well within our grasp, with recent research from UCL suggesting such an extension would need only a 2.3% GDP rise in taxes. The effect would be transformative and lay the foundation of a new age of innovation, social cohesion, and rebalanced labour relations. By shifting the responsibility for a satisfied demos from material consumption to a more relational basis, dependence on finance is reduced at the same time that costs are reduced through social wage substitutions. Until other societies replicate the model, the first movers benefit from substantial competitive advantage.

If human societies are to break the current mould that seems to lead inexorably to never-seen-before destructions, then it can only happen if a new model is established free from the implausible justifications of infinite growth on a finite planet, unrepayable debt, and magic money. Few countries have the present time luxury to consider these long term problems, less have the predisposition to question their own orthodoxies, and even fewer have the capacity and strength to embark on such a journey. Can anyone other than Britain take the lead? Can anyone afford for Britain not to take the lead?

{kind=link}

You must be logged in to post a comment.